Options spreads are often described as “defined risk” strategies — structured trades where the maximum gain and loss are known in advance. But real markets, especially around earnings and near expiration, can behave in ways that feel anything but predictable. This post breaks down a real Microsoft options trade that started as a credit spread sold near ATM before earnings for a net credit of $1.48 and turned into a powerful lesson in volatility, liquidity, and exit planning.

The Trade Setup — A Credit Put Spread

The position was a bull put credit spread on MSFT:

- Sold (short) 460 put

- Bought (long) 455 put

- Expiration: February 20

- Strike width: $5

- Net credit received: $1.48 ($148)

This spread was opened before earnings when the short strike was almost at-the-money.

Intent of the trade: Profit if MSFT stayed above 460 or at least did not fall significantly.

Risk profile:

- Maximum profit: $148 (credit received)

- Maximum loss: $5 − $1.48 = $3.52 per share ($352)

- Breakeven: 460 − 1.48 = $458.52

At entry, the short put was not ITM — it was sold nearly ATM. The primary risks were:

- The stock staying around the same price, allowing time decay to help slowly

- A downside move pushing the spread into the money

Earnings Didn’t Help

The expectation was that either:

- MSFT would hold steady or rise, allowing the spread to decay toward profit

- Or any volatility spike would fade after earnings

Instead, the stock moved unfavorably enough that the spread became in the money, but not decisively enough to immediately reach maximum loss.

This created the most uncomfortable scenario for a credit spread seller:

An ITM spread with time still remaining.

The Strange Pricing One Week Before Expiry

One week before expiration, the quotes to close the spread became puzzling:

- Spread to close showed $5.10 to $6.95

- At one point, even around $7.50

This was alarming because the maximum intrinsic value of a $5-wide spread at expiry should be $5.

Why a $5 Credit Spread Can Quote Above $5

Several factors explain this:

1. Bid-Ask Spread Distortion Between Legs

To close a credit spread, you must:

- Buy back the short put at the ask

- Sell the long put at the bid

If liquidity is thin, those prices can be far apart. The combined execution price can exceed the theoretical $5 width.

2. Liquidity Collapse Near Expiry

Deep ITM options often trade with poor liquidity because fewer participants remain active. Market makers widen spreads to compensate for risk.

3. Implied Volatility Skew

Post-earnings volatility does not normalize evenly across strikes. Different implied volatilities on each leg can distort the spread’s market price.

4. Early Assignment Risk

American-style options allow early exercise. The risk of being assigned on the short put pushes market makers to quote defensively.

5. Broker Display Mechanics

Many platforms show conservative “worst-case” close estimates using unfavorable leg prices rather than realistic midpoint fills.

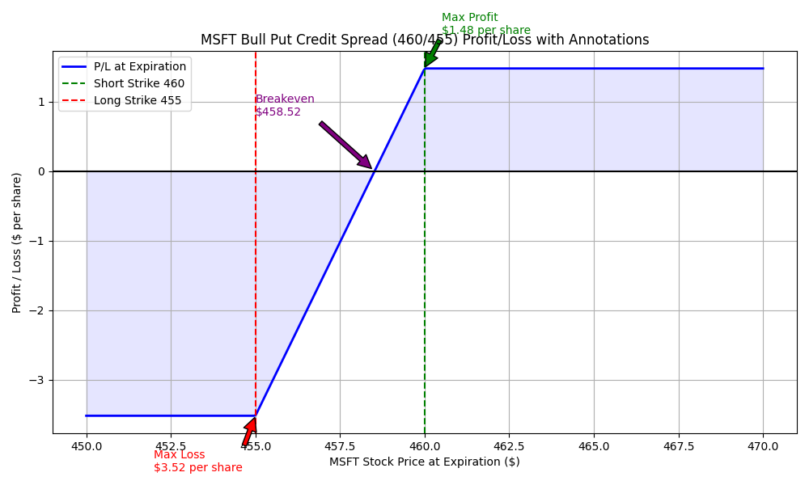

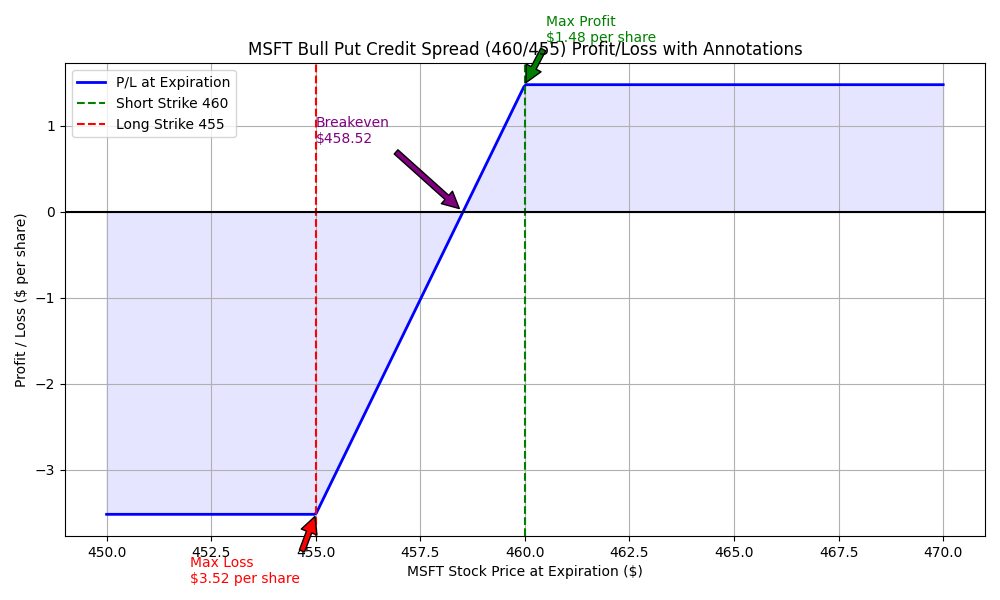

Visualizing the Payoff

To make this trade crystal clear, here’s the profit/loss chart for the MSFT 460/455 bull put credit spread:

Key points in the chart:

- Blue line: Profit/Loss of the spread at expiration

- Green dashed line: Short put strike (460)

- Red dashed line: Long put strike (455)

- Breakeven: 458.52

- Max Profit: $1.48 per share above 460

- Max Loss: $3.52 per share below 455

This chart visually shows why the spread’s real-market quote could appear “stretched” above the theoretical $5 in the week before expiry.

Close, Accept Assignment, or Execute?

Option 1 — Close the Spread

- Removes uncertainty

- Avoids assignment risk

- Requires careful limit orders to avoid overpaying

Option 2 — Allow Assignment

- Short 460 put could assign → buy 100 shares at $460

- Long 455 put allows selling at $455

- Result: maximum spread loss of $352 after accounting for the $1.48 credit

Option 3 — Manage Legs Individually

- Buy to close the short 460 put first (removes assignment risk)

- Then close or allow the long 455 put to expire

Best Action

For most traders, the cleanest solution is:

Close the spread using a limit order near the midpoint, or at minimum eliminate the short leg. Accepting assignment only makes sense if you are comfortable owning MSFT shares at an effective price near the breakeven and have the capital to do so.

Lessons Learned

- Selling Near-ATM Before Earnings Is High Risk

Even defined-risk spreads can behave unpredictably when earnings volatility is involved. - Liquidity Risk Can Override Theoretical Pricing

A spread may have a defined maximum loss, but exiting it can still be costly if markets become illiquid. - Always Plan the Exit Before Entry

Know in advance whether you will:- Close at a predetermined loss

- Roll the trade

- Accept assignment

Clear rules reduce stress during the final week.

Final Thoughts

This trade reinforces a critical truth about options trading:

Defined risk does not guarantee smooth execution.

A credit spread that looks simple on paper can become complex when volatility, liquidity, and assignment risk collide — particularly around earnings and expiration.

The real edge comes not just from choosing strategies, but from understanding how markets behave when trades move against you — and preparing for that scenario before entering.